Lite Access Technologies

a fundamental analysis

Symbol: Lite Access Technologies (CVE)

Share Price: CAD$0,68

Market Cap: CAD$35,8 Million

Lite Access Technologies: Share Price History

Source: Google

By Manuel Maurício

September 4, 2020

Introduction

Lite Access Technologies is a rather particular construction company specialized in laying optic fiber for the internet through an innovative method called micro-trenching.

During my previous life as an architect-turned-project manager, one of my responsibilities was to supervise the installation of really big (and expensive) windows in Brasil. If this doesn’t seem sexy, it’s because it isn’t. When you’re in a developing country, 8000 kilometers away from the factory and you need to install some of the largest glass panels in the world, things can get pretty difficult pretty quickly.

I know my way around in a construction site. And that’s precisely the reason why I’ve never invested in a construction company. In the construction business, everything that can go wrong will go wrong exactly at the wrong time. On top of that, the final work will be as good as the engineer who is supervising it (not to mention the dozens of sub-contractors and suppliers that must be coordinated). If he or she isn’t driven enough, you can be sure that the construction will take longer and it will cost more than planned (yes, they all do. But some more than others).

Business

With this intro, it is my pleasure to bring you a sort-of-construction company today. Lite Access Technologies is the pioneer in micro-trenching for the fiber industry.

The way you traditionally lay fiber is by using a backhoe to dig a trench, lay the fiber inside the trench and then close it with the same dirt that was previously removed and finish it up with a finishing such as asphalt or cement. Alternatively, the fiber can also be hanged from telephone poles, but due to the weather and the fees that must be paid to the telephone companies, the underground solution has been favoured over the aerial one.

The traditional digging takes time and creates a big mess. That’s why Lite Access Technologies developed a technique called micro-trenching. With a special blade, the company is able to make a cut just a few centimeters wide (without making a big mess), lay the micro-ducts, and then close it as in the traditional method. After the microducts are in place, the fiber will be blown through them.

Usually, these ducts have several sections so if there is the need for more fiber in the future, there is the possibility to blow more fiber. This is usually called future-proofing; something that couldn’t be done with the traditional copper cable (coaxial).

The advantages of micro-trenching are threefold. This process is 1) much cleaner, 2) faster, and thus 3) much cheaper than the typical trenching.

Now, before getting to the really exciting part, let’s talk about the company’s history.

Company's History

Lite Access Technologies was founded in 2004 by Mike Plotnikoff and Michael Priest (aka “The Two Mikes”). At that time, it was just a fiber optic and microduct manufacturing company. In 2015, they took it public. Somewhere around that time the two Mikes figured that there was money to be made by installing the fiber, not just selling it. In August 2015 they bought DSG communications, a company specialized in infrastructure.

At some point the company went to the UK where the internet network is pretty much outdated and where a massive investment is being made as we speak (more on that in a minute).

The company closed a big contract worth CAD$29 Million with GigaClear to bring full fiber broadband to up to 10.000 homes, investors got all fired up thinking that this was the contract that would lead the company to profitability, but then there were internal problems over at GigaClear. The whole management team was replaced, the new management team reassessed all the prior contracts, stopped giving work to Lite Access, Lite Access was pissed, but the contract was so badly written that there was nothing that Lite Access could do. It just ran out of work.

The most important thing for a construction company, especially a low margin one such as LTE is good contracts. Contracts that allow for constant workflow without any stops. That and several clients. Not just one.

In the meantime, a group of disgruntled shareholders that met on an online forum started sending letters to the Board of Directors complaining about the inaptitude of the Two Mikes to lead the company. The Board of Directors took notice, the two Mikes acquiesced and the search for a new CEO started with the help of a recruiting company. That’s how Carlo Shimoon was found. He came back from retirement to set things straight, but according to the man himself, he never thought he would find such a big mess. He took 6 months just to stop the bleeding of cash, which, truth be told, hasn’t been completely stopped yet.

From what I’ve been able to gather (h/t to my friend Trevor Trew from Veritas Vatillum), the reason why Carlo is still with the company is not because he loves it, but because he set out to – at least – straighten the boat. I don’t believe he will stick around for long. Who knows, maybe I’m wrong.

The UK opportunity (the exciting part)

Most people aren’t aware of this but the UK ranks as one of the worst countries in Europe in what relates to the internet infrastructure. I have several friend living there and they all tell me that Portugal has way faster internet than the UK.

In today’s world, with a lot of the computing power moving to the cloud and with 5G coming, full broadband is a major basic necessity. And the UK politicians know that. That’s why the Government is spending billions on upgrading the whole country’s internet infrastructure. They are connecting every single city, town and village with fiber. And there are hundreds of these cities and towns. That’s a massive endeavour which implies a huge deployment of contractors, engineers, construction workers and machinery.

Add to this the fact that there is a massive shortage of workers in the UK right now. These companies are hiring every single person they can, even ex-convicts and all.

When Carlo joined the team, he immediately had to deal with Gigaclear and tried to rewrite the previous contract in better terms, but with no success. He understood that he had to find another big client, ideally more than one. He started conversations with other players and in October 2019, CityFiber, one of the largest fiber infrastructure builders and fiber wholesalers in the UK, awarded Lite Access a contract for Fiber-to-the-Premises (FTTP) installation to over 28.000 homes in Lowestoft. Valued at CAD$20 Million, this was the first of three contracts that will probably change Lite Access forever.

In January 2020, CityFiber awarded Lite Access a second contract in Bury St. Edmunds for CAD$13 Million over two years, and in April 2020, CityFiber awarded a third contract in Cambridge for CAD$20 Million over 21 months.

These 3 contracts combined represent a total backlog of CAD$53 Million. The company is worth $36 Million today.

CityFiber is planning on investing £4 Billion to reach 8 billion homes by 2025. In 2020 alone, CityFiber is expected to award £1,5 Billion (with a B) worth of contracts. The opportunity here seems massive.

“Lite Access Technologies is a great example of this having shown they can deliver full fibre networks to both residents and businesses with the requisite care and quality, and we look forward to working with them for years to come.” James Thomas, Director of supply chain at City FIber

With such shortage of people and companies, if Lite Access doesn’t mess up with these first contracts, there is a great probability that CityFiber will award it new and larger contracts.

Right now, CityFiber has 9 construction partners announced on its website. If it distributes the £1,5 Billion through the 9 partners, each one of those partners will be awarded CAD$366M (£211 Million) on average. You can see how easily the share price could double, triple or much more in a short period of time, right?

The Warrants

I don’t want to bother you with the details and I apologize to the subscribers who are not into finance, but a brief explanation about the recent funding is of the order here. Those of you who wish to skip this part, just jump to the next session.

During the second quarter of 2020 – which for Lite Access runs from January through March – the company has financed itself through a Private Placement. A private placement is just like any other equity raise, the company issues new stock, but directly to a small number of chosen investors rather than through the stock market. The company raised $3,5 Million in exchange of roughly 7 Million units at $0,5 each.

Each unit consists of 1 common share and 1 Warrant. Warrans are used in Private Placements to sweeten the deal. They’re just options to buy shares at a pre-set price in the future. In this case, at $0,68 per share. This way, investors who paid $0,5, got 1 share right away and the right to buy another share at $0,68.

After the private placement, if the share price is above $0,5, investors can immediately cash in the difference by selling their newly issued shares in the open market. On top of that, if the share price is above $0,68 at some point in the future, the warrants allow them to buy new shares at $0,68 from the company and sell them in the open market, thus making a profit.

But – and there is always a but – the company had the right to accelerate the expiry date of the warrants in order to raise cash. This just means that investors must exchange their warrants for new shares units until the 11st of September rather than the previous set date of 2023.

The problem here is that the company has done this prior to an announcement of further contracts. This obviously isn’t a good strategy. It’s in the company’s interest to raise as much cash as it can. If investors see, say, a share price of $1 while they can exercise their warrants at $0,68, they will want to exercise the warrants. But if the share price is $0,68 or less, they might not exercise the warrants. Why would they? They can buy the shares for less than that in the open market.

These warrants will expire on September 11th, so it would be in the company’s interest to announce a new contract by then.

Financials

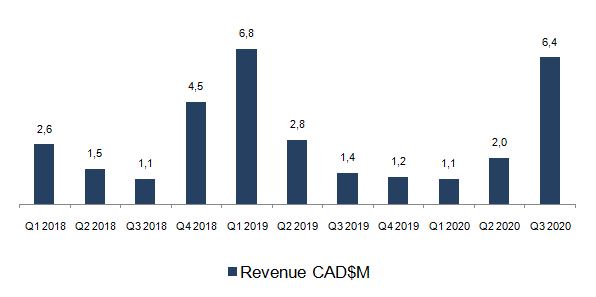

Turning now to the financials, we can clearly see the ramp up in 2018/19 and the subsequent debacle after the GigaClear “misunderstanding”.

Revenue, CAD$ Millions

Source: Company data

What we’re also able to see is the huge growth in revenue in the most recent quarter. I’ve talked to Rob Gamley from the Investment Relations and he has told me that the company didn’t reach full deployment rates in each city. Lowestoft was at full deployment rate, Bury St Edwards was ramping up, and Cambridge was starting. The company should be close to a “steady-state” in the 3 cities by the end of Q4 (September).

That means that we should expect revenue to be around $10 Million per quarter going forward which would mean total revenue for 2021 of around $40 Million. Rob has also told me that the (gross) margins should be in the range of 20% to 30% in a steady-state.

If we do a quick math, let’s say that in 2021 the company reaches $40 Million in revenue, $12 Million in gross profit (30% margin) and has operating expenses of $8 Million. That would be a profit of $4 Million. With 63 million shares outstanding, that would amount to $0,063 of earnings per share. At a PE ratio of 10x, that would mean a share price of $0,63. For the current backlog, the company seems fully valued right now.

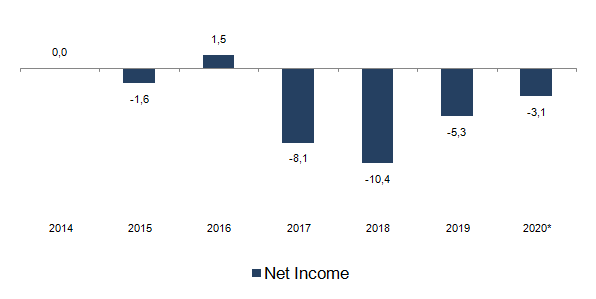

Net Income, CAD$ Millions

Source: Company data

The company has no debt on its balance sheet, and should be shored up with cash after the warrants get converted (if they get to be fully converted).

Risks

- Customer concentration

- This is a low-margin construction company with no profits yet. Everything is a risk.

Conclusion

I’ve started my research on Lite Access all fired up about the possibility of tripling my money in a short period of time. There is no doubt in my mind that that’s highly likely. In fact, the stock price has already gone up 10x in the past year…

… the company just needs to announce 1 or 2 more contracts and investors will come running.

As I was doing my research I was getting more and more aware that this is a lousy business with low margins, very low barriers to entry, highly dependent on one single customer, with high staff turnover where everything can go wrong and without proof of being able to keep profitable at a steady-state.

Although the opportunity here looks fantastic and there is a high probability that this turns out to be a very successful speculation, it’s just not for me. I wouldn’t be sleeping well if I were to buy it. One year from now, we might be seeing Lite Access Technologies being valued at multiples of its price today, but I’ll be watching from afar.

A final note of appreciation: As part of my research process, I like to talk to people who know more than I do about the industry that I’m researching. I must thank Ruben Guerreiro, a subscriber who works in the infrastructure building industry. He was of great help to me. Thank you Ruben.

Further research material

- Lite Access Technologies – An essential business in the booming UK telecom build (paywall protected)

- CityFiber announces 36 more cities and towns to benefit from fiber

- Conference Call with Trev Trew

- News and articles about the UK fiber roll out: 1, 2

DISCLAIMER

The material contained on this web-page is intended for informational purposes only and is neither an offer nor a recommendation to buy or sell any security. We disclaim any liability for loss, damage, cost or other expense which you might incur as a result of any information provided on this website. Always consult with a registered investment advisor or licensed stockbroker before investing. Please read All in Stock full Disclaimer.